The New Debt Restructuring Procedure – A Case Study

Legislation has recently been introduced into Parliament for the new debt restructuring process. The new process, which is only available for companies with debts less than $1 million, is intended to commence from 1 January 2021.

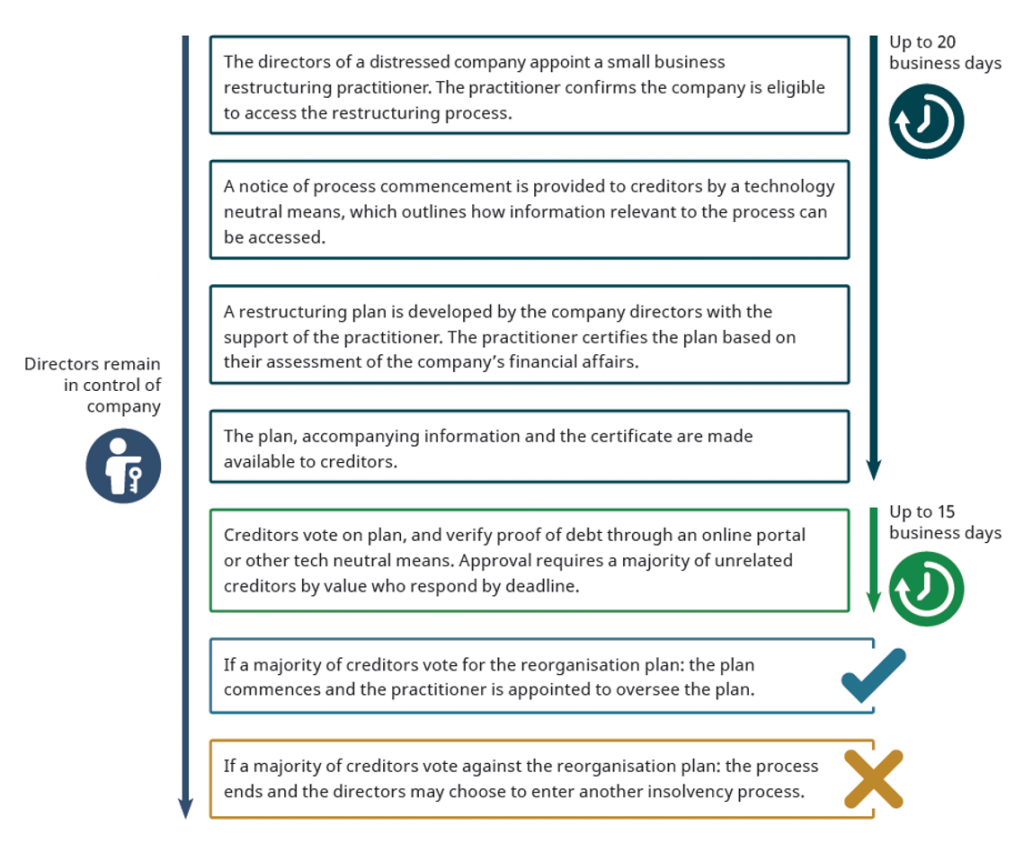

The new process will involve a “small business restructuring practitioner”, who must be a Registered Liquidator, helping the business prepare the plan, certify the plan to creditors and oversee disbursements once the plan is in place.

A period of 20 business days is proposed to allow for development of the plan.

While the practitioner is engaged in the restructuring process, there will be a moratorium on unsecured and some secured creditors taking actions against the company.

Creditors will then have 15 business days to vote on the plan. Employee entitlements that are due and payable must be paid out in full before the plan is voted on by creditors.

Here’s an example of how it will work:

Case study: Samantha’s Fitness Centre

Samantha owns and runs a popular fitness centre. During the early stages of the Coronavirus outbreak, patronage at the fitness centre drops sharply as people comply with health restrictions.

Once the measures were wound back, customers slowly returned. While income mostly returned to normal, Samantha’s business faces a financial crunch. Samantha had accrued significant debts while her business was in ‘hibernation’. These debts are due to be paid soon. When the temporary insolvency measures are removed in January 2021, Samantha worries about the risk that her business is trading while insolvent.

| Without access to the new restructuring process | With the new restructuring process in place | |

| Samantha researches some options for distressed businesses, but is wary of voluntary administration because of its cost. She is also concerned about the prospect of outside Administrators taking over the running of her business. She worries that the Administrators may choose not to operate the business, because the Administrators would be liable for debts incurred and the business has insufficient assets to cover these. Samantha continues to trade for a period. However, the debt burden becomes too great to bear, and she is eventually unable to make payments to her company’s creditors when they come due. Samantha has no choice but to place her business into liquidation. The fitness centre closes and its employees are laid off. Its creditors receive a proportion of the debts they were owed. | Samantha approaches Oracle Insolvency Services, who advise her to engage in the new restructuring process. Samantha identifies her company’s creditors and proposes a new repayment schedule through a restructuring plan. The small business restructuring practitioner looks at the company’s financial affairs and determines that the plan is workable. The plan is put to creditors, a majority of whom by value approve the plan. Samantha remains in control of her business throughout the process and is able to continue trading. The debts owed to creditors are paid back according to the terms of the plan. Samantha’s employees remain employed and her business trades on. Although the creditors receive a reduced payment versus the amount they were initially owed, they receive more than if Samantha were to put her company into liquidation. |

But importantly:

It should be noted that the proposed legislation requires a company under restructuring to:

- pay all “employee entitlements”, other than contingent entitlements; and

- lodge all outstanding activity statements and tax returns with the ATO.

“Employee entitlements” are defined to include wages, superannuation, leave and retrenchment payments.

Company directors considering the new restructuring procedure should start planning now, by ensuring employee entitlement payments and ATO lodgements are up-to-date.